Nonprofit Meeting Minutes Best Practices

The Maine Nonprofit Corporation Act requires minutes to be kept for every meeting of a nonprofit Board, its members, and committees with authority of the Board.1 Although it isn’t required, minutes may also be taken at other committee meetings to support the nonprofit’s institutional memory. Just like other important institutional documents, such as the nonprofit’s articles of incorporation, bylaws, and tax-exempt determination letter, minutes should be kept permanently and in a safe place, either digitally, physically, or both. Furthermore, it is important to have procedures in place to approve minutes. These normally involve distributing the draft minutes to meeting attendees before the next meeting so that inaccuracies may be corrected in advance of approval at that next meeting.2

Minutes are one of the ways by which a nonprofit organization and its board and officers can evidence compliance with not only the nonprofit’s own governing documents, but also state and federal law.3

Nonetheless, minutes need not be a transcript of a meeting. Instead, minutes should provide a clear and objective summary explanation of what occurred and document actions taken. For example, it is a best practice for minutes to include the following:

the meeting’s date, time (beginning and end), and location;

the names of directors/committee members/members in attendance and those that are absent;

names of guest attendees;

whether a quorum exists;

whether the meeting is regular or special;

whether attendees depart and re-enter;

a summary of key points from any reports given;

action items and/or resolutions; and

Secretary’s signature once minutes are approved.

Specifically in terms of formal votes on whether the Board will take action in response to a motion, special care should be taken to record the following:

description of motion made and by whom;

who seconded the motion (if in fact seconded);

brief summary of debate; and

voting results, together with the names of dissenters, abstainers, and recusals or whether the motion was tabled.

If the action involves potential or actual conflicts of interests, then the minutes must document how the conflicts were handled (i.e., according to the nonprofit’s conflict of interest policy based on applicable law).4 Similarly, if the action involves setting executive compensation, the minutes should include the information recommended by the IRS here.

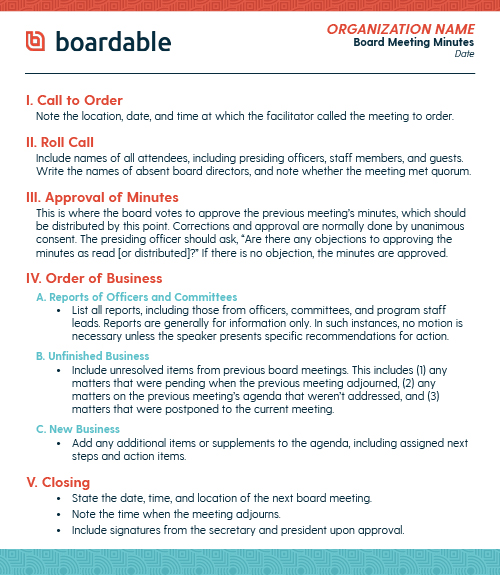

Though there is no required way to organize the above, following a template like that found here may be useful, and it may also be used as a template for meeting agendas.

{kind=link}

Lastly, because many Maine nonprofits do not qualify as a public agency or political subdivision for purposes of the State’s Freedom of Access Act, they are not required to share meeting minutes with, nor must they open their meetings to, the general public.5 Nonetheless, the Board may decide to do so in the name of transparency and to foster good will. This said, voting members of nonprofits do have the right to inspect minutes for “the purpose of enabling the member to fulfill duties and responsibilities conferred upon members by the articles of incorporation or the bylaws of the corporation or by law.”6 As a result, when drafting meeting minutes, it is important to be cognizant of sensitive and confidential issues. Such issues may be discussed in an “Executive Session,” which is a separate, confidential portion of a meeting. Though separate and confidential, notes of the Session should still be taken with any actions or votes noted, marked as confidential, kept separate from the meeting’s regular minutes, and distributed only to those present at the Session.

We Serve Nonprofits

If your nonprofit is seeking guidance with maintaining and keeping accurate corporate records, including nonprofit meeting minutes, please contact us to learn more.

[1] 13-B M.R.S. § 715(1).

[2] IRS Form 990 Part VI, Section A, Question 8 asks if the organization contemporaneously documents the meetings or actions by its “governing body” and “committees with the authority to act on behalf of the governing body.” IRS, 2020 Form 990 Return of Organization Exempt From Income Tax 6 (2020), https://www.irs.gov/pub/irs-pdf/f990.pdf. Form 990’s Instructions define contemporaneous as “the later of (1) the next meeting of the governing body or committee (such as approving the minutes of the prior meeting), or (2) 60 days after the date of the meeting or written action.” IRS, 2020 Instructions for Form 990 Return of Organization Exempt From Income Tax 23 (2020), https://www.irs.gov/pub/irs-pdf/i990.pdf. Meeting minutes may also be certified by a Secretary’s Certificate stating that the minutes are accurate. See 13-B M.R.S. § 1305.

[3] See 13-B M.R.S. § 1305; IRS, Internal Revenue Manual § 4.75.11.8.3 (2017) (the IRS may request meeting minutes and attachments, exhibits, and reports mentioned in the minutes when auditing a nonprofit), https://www.irs.gov/irm/part4/irm_04-075-011#idm140079823228928.

[4] See 13-B M.R.S. § 718.

[5] See e.g., Turcotte v. Humane Soc’y Waterville Area, 2014 ME 123, 103 A.3d 1023.

[6] 13-B M.R.S. § 715(1).

This is a site offering non-comprehensive commentary. It is not an attempt to provide legal advice. This blog may be construed as an advertisement, but should not be construed as legal advice or a legal opinion on any specific facts or circumstances, nor does it create attorney-client privilege.